Compound interest explained in one sentence: it is what happens when your money earns money, and then that new money starts earning money too. At first, it can feel almost boring. A few dollars of interest here, a slightly higher balance there. But give the math enough time, and the curve starts to bend upward in a way that feels less like arithmetic and more like momentum.

That is the quiet magic of compound interest. Small differences in interest rate, time, fees, and consistency do not stay small forever. Over long periods, they multiply. A one-percentage-point difference can become tens of thousands of dollars. Starting ten years earlier can matter more than trying to contribute much more later. A tiny fee that seems harmless in year one can quietly eat a surprising amount of growth by year forty.

This article is a friendly math guide, not financial advice. The goal is to show why compound interest matters, how the formula works, and why the phrase “start early” is not just motivational poster wisdom. It is math.

Compound Interest Explained: The Basic Idea

Simple interest is interest paid only on the original amount. If you put $1,000 somewhere that pays 5% simple interest per year, you would earn $50 each year. After ten years, you would have the original $1,000 plus $500 in interest, for a total of $1,500.

Compound interest works differently. With compound interest, the interest gets added to the balance. The next round of interest is calculated on the larger balance, not just the original amount. In year one, your $1,000 earns $50 and becomes $1,050. In year two, 5% is applied to $1,050, not $1,000, so the interest is $52.50. That extra $2.50 is not dramatic, but it is the beginning of the snowball.

The key idea is that compounding rewards time. The early years look modest because the base is still small. The later years are where the growth becomes more obvious because the base has become much larger. This is why compound interest often feels slow at first and powerful later.

The Formula: Why the Curve Bends Upward

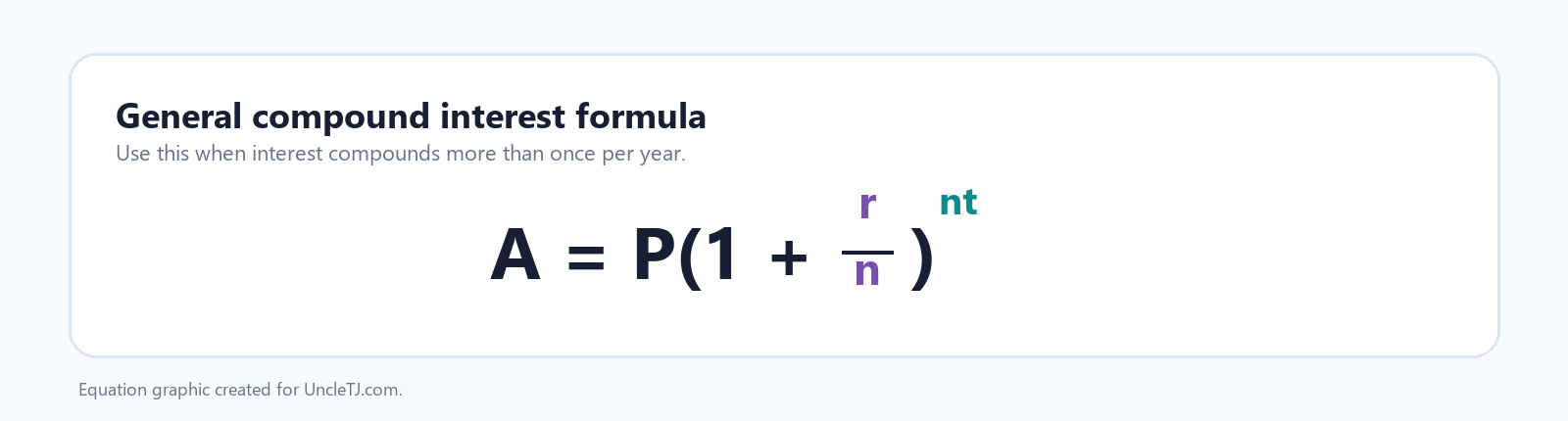

The standard compound interest formula is:

- A is the final amount.

- P is the principal, or starting amount.

- r is the annual interest rate as a decimal.

- n is the number of times interest compounds per year.

- t is the number of years.

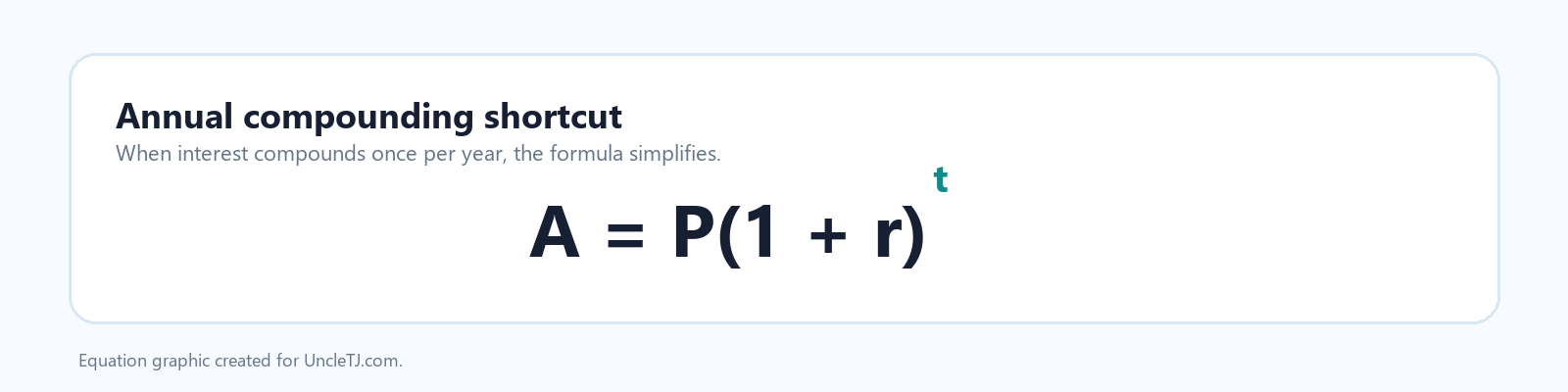

If interest compounds once per year, the formula becomes simpler:

That little exponent is the star of the show. It means time does not just add to the result. Time raises the growth factor again and again.

For example, $10,000 at 7% for one year becomes $10,700. After two years, it becomes $10,000 multiplied by 1.07 twice, or about $11,449. After forty years, it becomes about $149,745. You did not earn the same $700 every year. The annual growth got larger because the balance got larger.

This is the mathematical reason compound interest creates a curve instead of a straight line. A straight line says, “add the same amount each period.” A compounding curve says, “grow by a percentage of the new total each period.”

Compounding Frequency: Annual, Monthly, and Daily

Another detail in the formula is n, the number of times interest compounds each year. Annual compounding means interest is added once per year. Monthly compounding means interest is added twelve times per year. Daily compounding means it is added every day.

More frequent compounding usually helps the balance grow a bit faster, because interest gets added sooner and then starts earning interest itself. But for most everyday examples, the difference between monthly and daily compounding is smaller than the difference created by time, contribution habits, fees, and the interest rate itself.

That is useful to remember. People sometimes obsess over tiny compounding-frequency differences while ignoring bigger levers. A higher contribution rate, a lower fee, or five extra years of patience will usually matter more than whether interest compounds monthly or daily.

Inflation also matters. If your money grows by 7% but prices rise by 3%, your purchasing power did not really grow by the full 7%. Economists call the after-inflation result a real return. Compound interest can build impressive nominal balances, but what those dollars can buy in the future is part of the real-world story too.

Small Rate Differences Become Huge Over Time

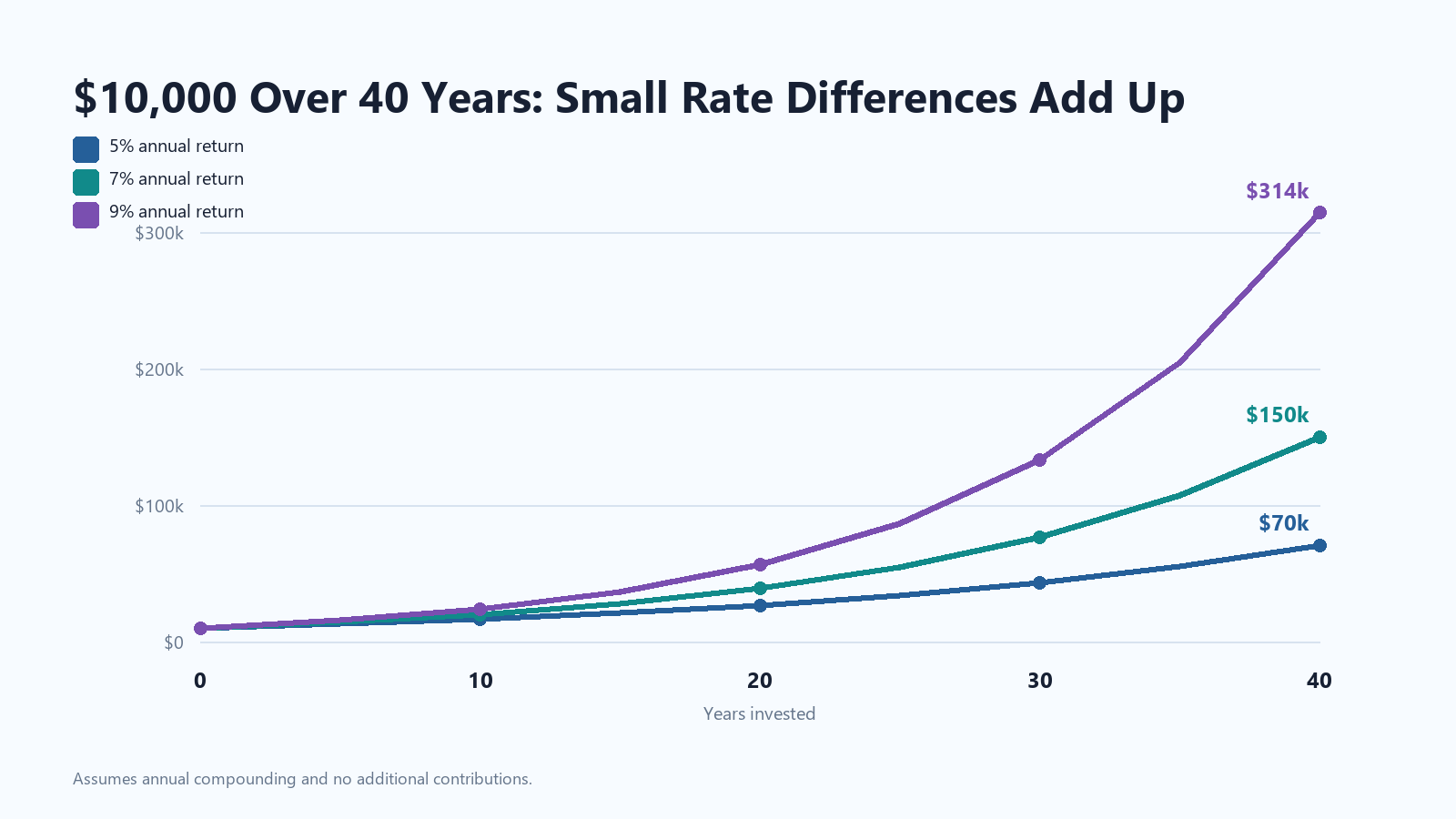

One of the easiest ways to see the power of compound interest is to compare different rates over the same period. Suppose you start with $10,000 and leave it alone for 40 years. No extra contributions, no withdrawals, just annual compounding.

The chart below compares 5%, 7%, and 9% annual growth. These are examples, not predictions. Real investments move up and down, and no return is guaranteed. But as a math example, the pattern is clear: the gap between rates gets wider over time.

| Annual rate | Starting amount | After 40 years |

|---|---|---|

| 5% | $10,000 | About $70,400 |

| 7% | $10,000 | About $149,700 |

| 9% | $10,000 | About $314,100 |

Notice how the 9% result is not just a little better than the 7% result. It is more than twice as large after forty years. That is why fees, tax drag, return differences, and contribution delays matter so much over long periods. Small differences do not stay small when they are compounded.

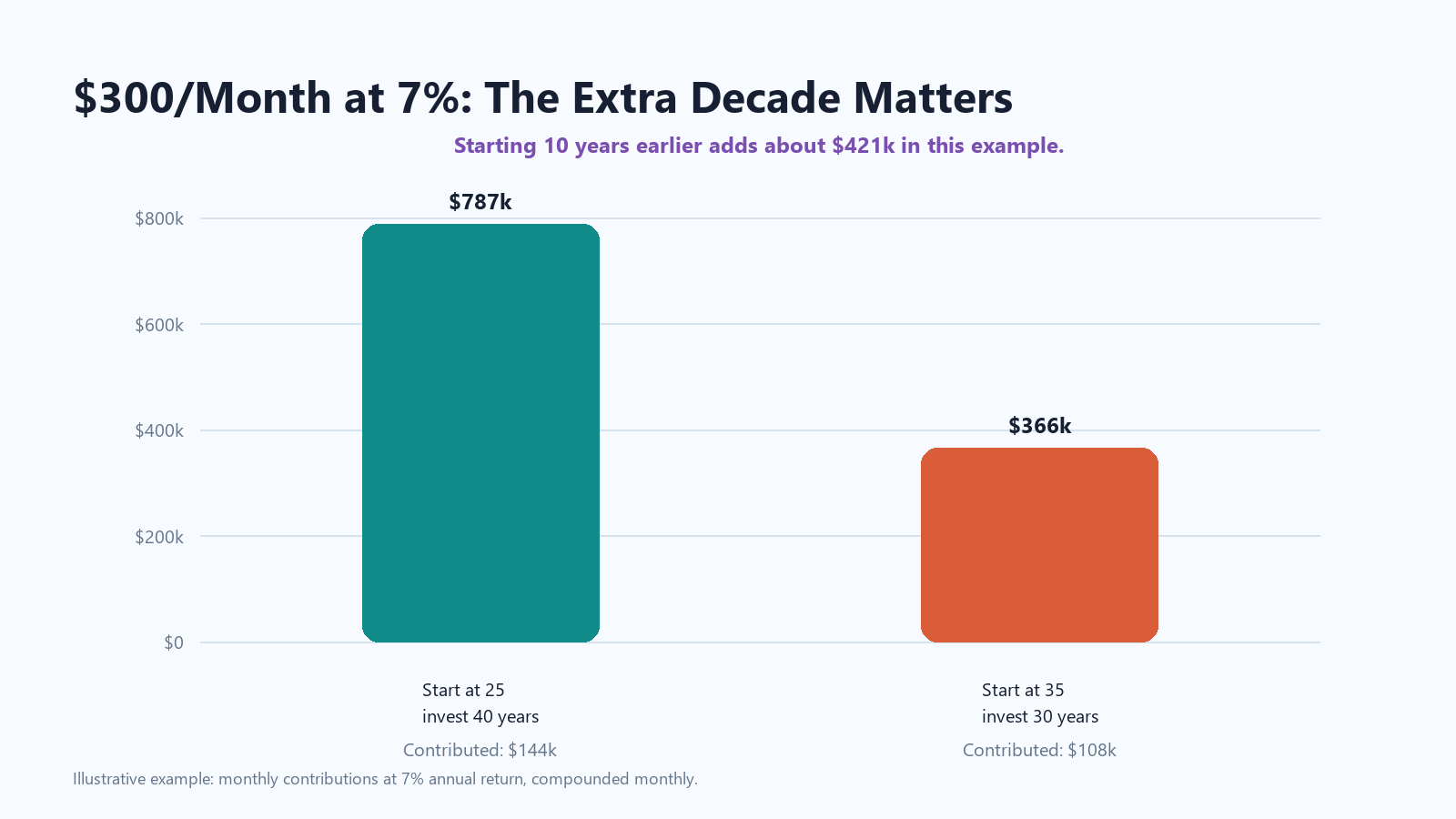

Starting Earlier Beats Trying to Catch Up Later

Compound interest also explains why starting early can be so valuable. Imagine two people who both invest $300 per month and earn an illustrative 7% annual return, compounded monthly.

- Person A starts at 25 and invests for 40 years.

- Person B starts at 35 and invests for 30 years.

Person A contributes $144,000 over the full period. Person B contributes $108,000. The difference in contributions is $36,000, which is meaningful. But the ending balance difference in this example is much larger because Person A also gets an extra decade of compounding.

The chart below shows the math. In this example, starting at 25 grows to about $787,000, while starting at 35 grows to about $366,000. The extra decade adds roughly $421,000, even though the extra contributions are only $36,000. That is time doing the heavy lifting.

This is not a reason to feel bad if you did not start early. It is a reason to respect the clock. The second-best time to understand compound interest is whenever you are reading this sentence. The math still works from here.

The Rule of 72: A Quick Mental Shortcut

The Rule of 72 is a simple way to estimate how long it takes money to double. Divide 72 by the annual growth rate. The answer is the approximate number of years it takes to double.

- At 6%, money doubles in about 12 years because 72 divided by 6 is 12.

- At 8%, money doubles in about 9 years because 72 divided by 8 is 9.

- At 12%, debt can double in about 6 years if the interest is left alone.

The Rule of 72 is not perfect, but it is useful because it turns compounding into something you can feel quickly. Higher rates do not just add more growth. They shorten the doubling time. That is wonderful when you are earning interest and painful when you are paying it.

Compound Interest Can Work For You or Against You

Compound interest is often discussed as an investing superpower, but it is really just math. The same math can help or hurt depending on which side of the interest rate you are on.

When you save or invest, compounding can help your balance grow. Savings accounts, certificates of deposit, retirement accounts, bonds, dividend reinvestment, and long-term investment portfolios can all involve some form of compounding. The exact results depend on the rate, fees, taxes, risk, and time horizon.

When you borrow, compounding can work against you. Credit card balances, unpaid interest, certain loans, and late fees can grow faster than expected if the balance is not reduced. This is why high-interest debt can feel so hard to escape. The balance is not just sitting there. It may be growing while you are trying to catch up.

That is the big practical lesson: compounding rewards consistency on the asset side and punishes delay on the debt side. If you can get compound interest working for you, time becomes a helper. If high-interest debt is compounding against you, time becomes pressure.

Three Small Differences That Matter More Than They Seem

The math of compound interest makes three everyday decisions especially important.

1. The rate matters

A higher return, a lower loan interest rate, or lower fees can create a big long-term difference. One percentage point may not sound dramatic, but over decades it can separate two outcomes by a large amount.

2. The timeline matters

More time gives compounding more rounds to work. This is why early contributions can be so valuable. Even small amounts can become meaningful if they are given enough time.

3. The habit matters

Most people do not build wealth from one perfect decision. They build it from repeated decisions: saving a little, investing regularly, avoiding unnecessary high-interest debt, reinvesting growth, and letting the math keep working.

How to Use Compound Interest in Real Life

Here is a practical way to turn the math into action.

- Use a calculator. Investor.gov has a helpful compound interest calculator that lets you test starting amounts, monthly contributions, rates, time, and compounding frequency.

- Compare scenarios. Look at what happens if you start five years earlier, increase a contribution, reduce a fee, or change the rate assumption.

- Watch fees. Fees also compound, but in the wrong direction. A small annual fee difference can reduce the amount that stays invested and grows.

- Prioritize high-interest debt. If the interest rate on debt is high, the compounding math may be working against you faster than your savings math can work for you.

- Stay realistic. Compound interest examples are clean. Real life includes job changes, emergencies, inflation, taxes, market swings, and human behavior.

Compound interest is not a get-rich-quick trick. It is more like a get-patient-slowly advantage. The power comes from giving the formula enough time and not interrupting it too often.

Try the Compound Interest Calculator

Want to see the math move? Enter a few numbers below and watch how the projected balance changes as time, return, and contributions interact.

Quick FAQ: Compound Interest Explained

What is compound interest in simple terms?

Compound interest is interest earned on both the original amount and the interest that has already been added. It is interest on interest.

Why does compound interest get so powerful over time?

Because each round of growth applies to a larger balance. The longer the money compounds, the more the later years are driven by previous growth.

Is compound interest only about investing?

No. It can apply to savings, investments, loans, credit cards, and any situation where interest gets added to a balance and then affects future interest.

What is the biggest lesson from compound interest?

The biggest lesson is that small differences can become huge when repeated over enough time. Rate, fees, time, and consistency matter more than they appear to at first.

Final Thought

Compound interest is one of those ideas that sounds simple until you actually run the numbers. Then it becomes a little startling. The math says that time is not just a background detail. Time is one of the main ingredients.

If you remember nothing else, remember this: compounding magnifies differences. A little more time, a little lower cost, a little better rate, or a little more consistency can turn into a very different future number. That is why compound interest deserves its reputation. It is not loud, but it is relentless.

Sources and Further Reading

- Investor.gov: Compound Interest glossary

- Investor.gov: Compound Interest Calculator

- Related reading on UncleTJ.com: Roth IRA Calculator, Real-World Budgeting, and How to Use ChatGPT-5 for Personal Budgeting.